As Congress returns from its August recess, the Senate is expected to consider raising Chapter 13 debt limits—a move that practitioners say would ease pressure on consumers from housing costs and student loans.

The proposal, one of 600 amendments to the national defense bill, would temporarily adjust eligibility for people with regular income who want to reorganize debts in bankruptcy. It also replaces $1.58 million and $526,000 caps for secured and unsecured debt, respectively, with a single $2.75 million ceiling.

The amendment introduced July 31 by Senate Judiciary Chair Chuck Grassley (R-Iowa) and Ranking Member Dick Durbin (D-Ill.) would restore higher debt limits for individual filers and small businesses under Subchapter V, a Chapter 11 section created in 2019.

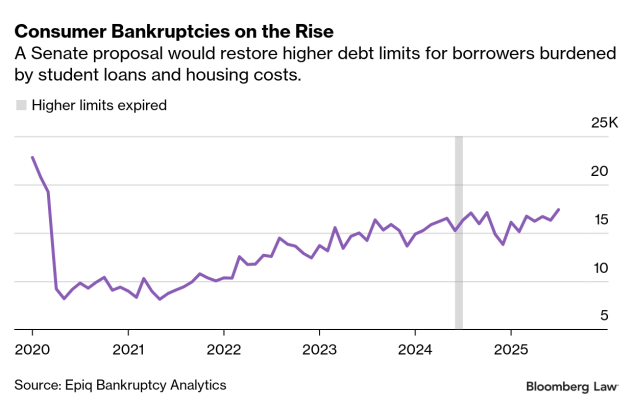

Increased caps expired last June after temporary pandemic-related adjustments, and the amendment would be retroactive for cases that started when the limits lapsed.

The proposal would allow filers in high-cost states, such as New York and California, and those with large student loans or medical debt, to qualify for Chapter 13 relief, consumer bankruptcy attorneys said.

“The people most affected are in higher cost-of-living cities, where mortgage debts for houses in Los Angeles, San Francisco, or New York aren’t uncommon to be over a million dollars,” said Andrew C. Walker, managing partner at Walker & Walker Law Offices. “Farmers also face that issue because mortgages against farms have a very high dollar amount.”

Attorneys and policy analysts said the lower debt limits block access to bankruptcy relief, since Chapter 11—although it has no debt ceilings—comes with fees, and Chapter 7, also without limits, doesn’t help those seeking to keep assets like homes.

“This bipartisan amendment will restore the ability for families to get much needed relief from unaffordable mortgages, medical debt, and student loans, so that they can get back on their feet and invest in their future,” Durbin said in a statement.

A previous bill by Durbin to extend the heightened limits stalled due to opposition from Sen. Rand Paul (R-Ky.), but proponents see a chance this session.

Any other pushback would likely come from those who generally oppose the use of bankruptcy as a tool.

“What critics of this proposal say is, ‘We just don’t like bankruptcy in general. People shouldn’t be able to discharge their debts, and they should have to pay it back no matter what,’” Walker said.

‘Obsolete’ Limits

Michelle Bass of Wolfson Bolton Kochis PLLC said pre-Covid-19 limits were “obsolete, arbitrary gatekeepers” that affect wage earners and business owners.

“With inflation, the rising cost of goods, labor, and services, I have come across many individuals who don’t qualify for Chapter 13 or Subchapter V solely due to the debt limits,” Bass said.

The amendment would also increase the small business ceiling to $7.5 million from roughly $3 million.

A regular consumer won’t opt for liquidation or Chapter 11, said John Rao, a senior attorney with the National Consumer Law Center—especially if they want to keep property.

“Chapter 11 isn’t likely just because of the cost involved, particularly if you’re talking about someone who is truly just a consumer,” Rao said. “It’s possible they could file Chapter 7, but if they were looking to Chapter 13, it’s likely not going to provide the relief they were hoping for.”

Chapter 13 filings have risen this year. As of July, the monthly average stood at 16,362, according to Epiq Bankruptcy Analytics. Liquidations are also climbing amid high interest rates, record credit card debt, and resumed student loan collections.

Practitioners said increasing the debt limits won’t open the floodgates for debtors to abuse the bankruptcy process.

“If abuse is suspected, objections and motions to dismiss cases are filed, so abuse won’t be an issue with the higher debt limits,” said Linda B. Gore, former president of the National Association of Chapter 13 Trustees.

Category Disputes

Unsecured debt typically includes credit cards and student loans, and mortgages are usually considered secured debt. However, the separate caps have sparked disputes over debt classification, which can derail Chapter 13 cases.

In the 2016 bankruptcy of Stanley Boyd Green, an ex-spouse moved to dismiss Green’s case, claiming he omitted obligations that pushed his unsecured debts over the limit. Green deeded the former marital residence to his ex, rendering a Wells Fargo mortgage unsecured for him even though he remained liable for the full balance, she argued.

The court found he exceeded the caps and dismissed the Chapter 13 case.

“From a policy perspective, we try to avoid unnecessary litigation because this increases the cost for the debtor,” Rao said. “The debtor may not even try to file, or an attorney might look at the case and say, ‘There’s going to be litigation over this, it will cost you this much.’”

Walker said litigation is sometimes necessary when creditors disagree on amounts owed, especially for claims like emotional distress or business losses.

SBA Loan Guarantors

Economic pressures on businesses can also affect people who personally guaranteed SBA loans after the pandemic.

“The SBA loans were very popular back in 2021 and 2022, and people owe well over $300,000 to $500,000,” said Patrick L. Cordero, a Florida bankruptcy attorney. “Most businesses don’t succeed, especially restaurants and mom-and-pop stores, and they are stuck with a debt they can’t pay.”

The SBA inspector general reported in 2023 that the average 7(a) loan, the agency’s primary business loan program, grew to about $681,000 in fiscal 2021—a 28% increase from the previous period.

Defaults were unusually low due to pandemic relief, but the winding down of the loan programs and rising interest rates increased repayment risks for borrowers and financial exposure for the SBA.

“If Congress truly intended for these avenues of debt relief to be available for consumers, small businesses, and their owners, then the debt limits should absolutely be increased,” Bass said.

To contact the reporter on this story:

To contact the editors responsible for this story:

Learn more about Bloomberg Law or Log In to keep reading:

See Breaking News in Context

Bloomberg Law provides trusted coverage of current events enhanced with legal analysis.

Already a subscriber?

Log in to keep reading or access research tools and resources.