Cryptoassets and anonymity go hand in hand, or at least that’s the general perception. Tax administrations are concerned that individuals aren’t paying the right amount of tax on their cryptoassets. There’s no question that not all cryptoasset investors may be paying tax, and a lack of information is no doubt part of an increased focus by tax administrations on introducing global tax transparency standards.

Some argue that transparency standards aren’t required, as blockchain forensic tools can trace transactions on a relevant blockchain. However, while the tools have been used to identify people involved in certain transactions, they can’t identify who is behind a transaction, as that information isn’t on the blockchain. This system works well for criminal investigations—for example, where there is fraud—but it isn’t sufficient for tax transparency.

Moreover, information on the blockchain also has limited use, as an individual’s tax liability is more than that one transaction; it’s the totality of all their transactions that’s required.

Historically, offshore bank accounts and banking secrecy were used to evade taxes as tax administrations struggled to gather information outside their jurisdiction. However, with the introduction of the first truly global tax reporting standard, the OECD’s Common Reporting Standard, this changed. Under the CRS, details of offshore bank account holders were shared by over a hundred tax administrations, although notably not including the US. It’s arguable whether the CRS has improved tax compliance, but it has led to a reduction of 11.5% in cross-border deposits in offshore financial centers.

Tax Reporting Standards

Tax administrations have been quieter than financial regulators, but they have been working in the background on how to apply similar standards as the CRS to cryptoassets to increase transparency. There are currently three main tax reporting standards to consider:

- The EU’s Directive on Administrative Cooperation 8 (DAC8)

- The OECD’s Crypto-Asset Reporting Framework (CARF)

- The US’s recently proposed rules for digital brokers

DAC8 is the first standard that has been agreed. Under this standard, cryptoasset service providers, or CASPs—broadly businesses that can facilitate the storage and/or the exchange of cryptoassets for their customers—will have to collect and transfer customer information such as name and address. They will also need to report on transactional activity, including details such as the name of the cryptoassets, the gross amount paid, received, the number of units, and number of transactions.

DAC8 requires non-EU CASPs to report transactions wherever they have an EU citizen as a customer. There are questions as to what the EU can do to enforce the gathering of this information from CASPS that are outside the EU, and what it will do if a CASP doesn’t collect the required information.

All EU member states will be required to implement the standard into their legislation by Dec. 31, 2025 and CASPs have to comply with the reporting obligations from Jan. 1, 2026.

The OECD’s CARF was the first international standard to be developed with the purpose of reporting on cryptoassets. Negotiations started informally in 2019 with the standard being agreed in 2022, although it has yet to be ratified. This appeared to be a priority at the recent G-20 conference in New Delhi.

One of the main differences from DAC8 is the potential scope of the standard in the number of jurisdictions that could be included. For example, the CRS has over 100 jurisdictions that are party to the standard, meaning it’s possible that CARF could have a similar number of jurisdictions participating.

In terms of timescale for adoption, CRS came into effect on Jan. 1, 2016 (for early adopters) after the request for the standard was agreed in 2014. Therefore, if ratified, CARF could come into effect potentially as early as 2026 onward, with the first exchange of information in 2027.

The final standard is the proposed regulation announced on Aug. 25 for the reporting of cryptoassets (termed “digital assets’’) in the US. The US proposal is very detailed and will also be extraterritorial, further increasing demands on CASPs to keep up to date on the reporting requirements for their customers. This is at present only a proposal, and the US Treasury and IRS will need to consider the comments from stakeholders, meaning that implementation may be some time away.

The US hasn’t yet made any public announcement on ratifying the CARF agreement and the proposal doesn’t confirm if the US will join the agreement. If the US doesn’t ratify CARF, it won’t be able to access information from the other members. If the US does join CARF, the IRS will have to gather the information in the proposal to meet the CARF obligations.

More Obligations Than Ever

It’s clear there is a global desire to share information on cryptoasset transactions, and in the near future, CASPs and individuals are going to be affected by one of the standards.

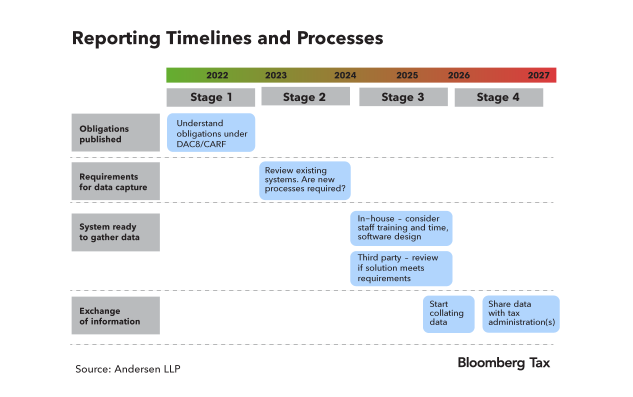

With the increasing regulatory demands on CASPs, they must keep abreast of global developments. Over the next few years, the challenge will be to ensure that they start putting systems and processes in place to meet their obligations. The infographic below indicates the timelines and processes CASPs should consider.

Many CASPs are concerned about the increasing regulations and how they can keep pace. This is particularly true for CASPs starting up—their concerns being that they will have fewer and less experienced staff than established CASPs, putting them at an economic disadvantage.

For individuals, increasing tax transparency means that tax administrations will have more information than ever before. In the UK, the potential change to the tax return and information from CARF will make it more evident if cryptoassets haven’t been declared and it’s likely this will lead to more investigations and exposure to penalties. There could certainly be consequences if taxpayers haven’t been keeping up to date with their tax returns.

The message from tax authorities is clear: Cryptoassets are firmly on their radar, making it more important than ever to report all crypto activities.

This article does not necessarily reflect the opinion of Bloomberg Industry Group, Inc., the publisher of Bloomberg Law and Bloomberg Tax, or its owners.

Author Information

Zoe Wyatt is partner and head of crypto and digital assets with Andersen.

Dion Seymour is crypto and digital assets technical director with Andersen.

We’d love to hear your smart, original take: Write for us.

Learn more about Bloomberg Tax or Log In to keep reading:

See Breaking News in Context

From research to software to news, find what you need to stay ahead.

Already a subscriber?

Log in to keep reading or access research tools and resources.