The Canadian business community has feared that each budget tabled by the Liberal government since 2015 would see a proposed increase to the capital gains rate. While the most recent federal budget doesn’t change the ordinary capital gains tax rate, it includes a less publicized change to the alternative minimum tax. That change effectively increases the tax rate on capital gains for many Canadians starting in 2024.

The AMT is a parallel tax calculation for individuals permitting fewer deductions, exemptions, and tax credits than under ordinary income tax rules. Individuals must pay the greater of their ordinary income tax and the AMT for the year. Unlike in the US, where the AMT has been publicly debated for decades, the AMT in Canada is largely ignored, as it previously applied in only very limited circumstances.

The federal AMT applies at a flat rate of 15% with a basic exemption of C$40,000 (about $30,000). The 2023 federal budget proposes to:

- Increase the federal AMT rate to 20.5% (in addition to the provincial minimum taxes);

- Expand the AMT base by, among other measures, increasing the capital gains and stock option inclusion rates for AMT purposes; and

- Raise the basic exemption amount to an estimated C$173,000 ($129,700).

These changes go beyond the proposals in the Liberals’ 2021 election platform to “create a minimum tax rule so that everyone who earns enough to qualify for the top bracket pays at least 15% each year.” They amount to what is essentially a hidden tax increase on many capital gains and stock option benefits. Taxpayers earning a significant portion of their income from capital gains or stock option compensation could be subject to increased AMT liability starting next year.

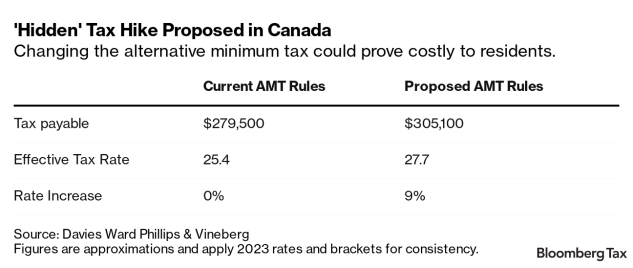

The following table shows the estimated impact of the AMT changes on an Ontario resident individual who earns employment income of C$100,000 and realizes a capital gain of C$1,000,000 that doesn’t qualify for the lifetime capital gains exemption.

The proposed AMT changes are estimated to increase this hypothetical taxpayer’s effective tax rate by approximately 9%. Taxpayers who realize larger capital gains likely would see more significant tax increases.

Additional tax paid under the AMT generally can be carried forward for seven years and credited against ordinary income tax. Accordingly, if an individual usually earns ordinary income that is taxed at the top marginal rate, AMT arising from capital gains likely can be carried forward and used in later years to reduce tax payable in those years.

If the AMT arises from extraordinary circumstances, such as a Canadian entrepreneur who realizes a capital gain on the sale of their business, the taxpayer may never be in a position to use the AMT credit, and the AMT could be a real and material cost.

The proposed measures will adversely impact many Canadian employees receiving stock option compensation—particularly where the benefit arises on a sale of a business, as the full benefit associated with stock options will now be included in the AMT base. Stock options remain a key compensation tool for start-up businesses in Canada and have helped to lessen the impact of Canada’s high marginal tax rates on attracting and retaining key employees to work in Canada’s tech sector. If the AMT makes stock options less attractive, this may hinder the ability of Canadian start-ups to attract and retain top talent.

The 2023 federal budget also proposes to include in the AMT base 30% of capital gains realized on donations of publicly listed securities. Taxpayers making charitable donations therefore may be liable to pay tax on capital gains in situations where the economic benefit of those gains flows to a registered charity. This tax treatment may dissuade some Canadians from making large donations to charities.

Historically, the AMT has been narrower in scope than its US counterpart. While the US AMT has been criticized for inadvertently impacting middle income taxpayers, the Canadian AMT has received comparatively little attention. With the newly proposed changes to the AMT, and the increased likelihood that it will adversely affect middle-class Canadians, it will be interesting to see whether the AMT will garner more attention going forward.

This article does not necessarily reflect the opinion of Bloomberg Industry Group, Inc., the publisher of Bloomberg Law and Bloomberg Tax, or its owners.

Author Information

Elie Roth is a partner with Davies Ward Phillips & Vineberg. He advises on all aspects of domestic and international tax planning, corporate reorganizations, mergers and acquisitions, and corporate finance.

Christopher Anderson is a partner with Davies Ward Phillips & Vineberg. He focuses on Canadian and international tax planning for investment funds, financial institutions, pension funds, mining companies and high-net-worth individuals.

Ryan Wolfe, an associate with Davies Ward Phillips & Vineberg, has assisted clients on a range of tax matters, including domestic and cross-border tax planning, mergers and acquisitions and tax dispute resolution.

We’d love to hear your smart, original take: Write for us.

Learn more about Bloomberg Tax or Log In to keep reading:

See Breaking News in Context

From research to software to news, find what you need to stay ahead.

Already a subscriber?

Log in to keep reading or access research tools and resources.